Share buybacks have always been a popular corporate tool in India — a way for companies to return surplus cash to shareholders, boost earnings per share, and signal confidence in their own stock. But the tax treatment of buybacks has been one of the most turbulent and frequently amended areas of Indian tax law. Just when investors thought they understood the rules, the government changed them. Again.

With the Income Tax Act 2025 in force from 1 April 2026, and the Finance Act 2026 introducing a crucial reset, the buyback taxation framework has undergone its most significant restructuring yet. If you are a retail investor, a company founder, a CA, or a finance professional, this blog explains exactly where things stand today — and what it means for you.

A Quick Primer: What Is a Share Buyback?

A share buyback (or stock repurchase) is a corporate action where a company buys back its own outstanding shares from existing shareholders, typically at a price higher than the prevailing market rate. Companies do this to:

- Return surplus cash to shareholders

- Reduce the number of outstanding shares and improve EPS

- Signal undervaluation of the stock

- Provide a tax-efficient exit route to shareholders

In India, buybacks by listed and unlisted companies are primarily governed by Section 68 of the Companies Act, 2013. For listed companies, SEBI's Buy-Back of Securities Regulations, 2018 also apply.

The Three-Phase Evolution of Buyback Taxation in India

To fully appreciate the current regime, you must understand how buyback taxation has evolved through three distinct phases. This is not just history — it directly affects your tax positions and loss carry-forwards.

Phase 1: The Company Tax Era (Up to 30 September 2024)

Under the Income Tax Act 1961, and specifically under Section 115QA, buyback taxation was simple from the shareholder's perspective: it was the company's problem, not yours.

The company paid an additional income tax at 20% on the distributed income (buyback price minus issue price) at the time of the buyback. The shareholder, in turn, received the buyback proceeds completely tax-free under Section 10(34A) of the old Act.

This seemed clean and efficient, but it created a serious problem: tax-induced inequity. Shareholders who participated in the buyback got a tax-free exit; those who couldn't or didn't participate received nothing, while the company's tax liability was borne by all shareholders indirectly. SEBI flagged this inequity as one of the reasons it discontinued open-market buybacks through stock exchanges from April 2025.

Phase 2: The Deemed Dividend Disaster (1 October 2024 to 31 March 2026)

The Finance (No. 2) Act 2024 swung the pendulum sharply. Effective 1 October 2024, it abolished the company-level buyback tax and instead brought buyback proceeds into the dividend framework — specifically through Section 2(22)(f) of the Income Tax Act 1961, and subsequently reflected in Section 2(40)(f) of the Income Tax Act 2025.

Under this framework:

- The entire buyback consideration received by a shareholder was treated as a deemed dividend and taxed at the applicable income tax slab rate

- The cost of acquisition of the shares tendered was recognized as a capital loss under Section 69 of the Act 2025 (corresponding to Section 46A of the 1961 Act)

This created an absurd and deeply unfair situation. Consider this example: you bought shares at ₹10,000 and received ₹15,000 in a buyback. Your actual profit was only ₹5,000. But under the deemed dividend framework, you were taxed on the entire ₹15,000 at your slab rate — potentially 30% — resulting in a tax of ₹4,500. Your actual profit: ₹500. Meanwhile, your ₹10,000 capital loss sat in your tax return waiting to be offset against future capital gains — which many retail investors simply never have.

The uproar from investors, CAs, and industry bodies was immediate and unanimous. The government listened.

Phase 3: The Capital Gains Reset (From 1 April 2026 — Current Position)

The Finance Act 2026, by amending Section 69 of the Income Tax Act 2025, has fundamentally corrected the Phase 2 anomaly. Buyback proceeds are now treated as capital gains — not deemed dividends. This is the current law as of today.

The Current Framework: Buyback Taxation Under IT Act 2025 (as Amended by Finance Act 2026)

The Finance Act 2026 has introduced a two-tier system — one rule for retail/ordinary investors, and a separate, stricter rule for promoters.

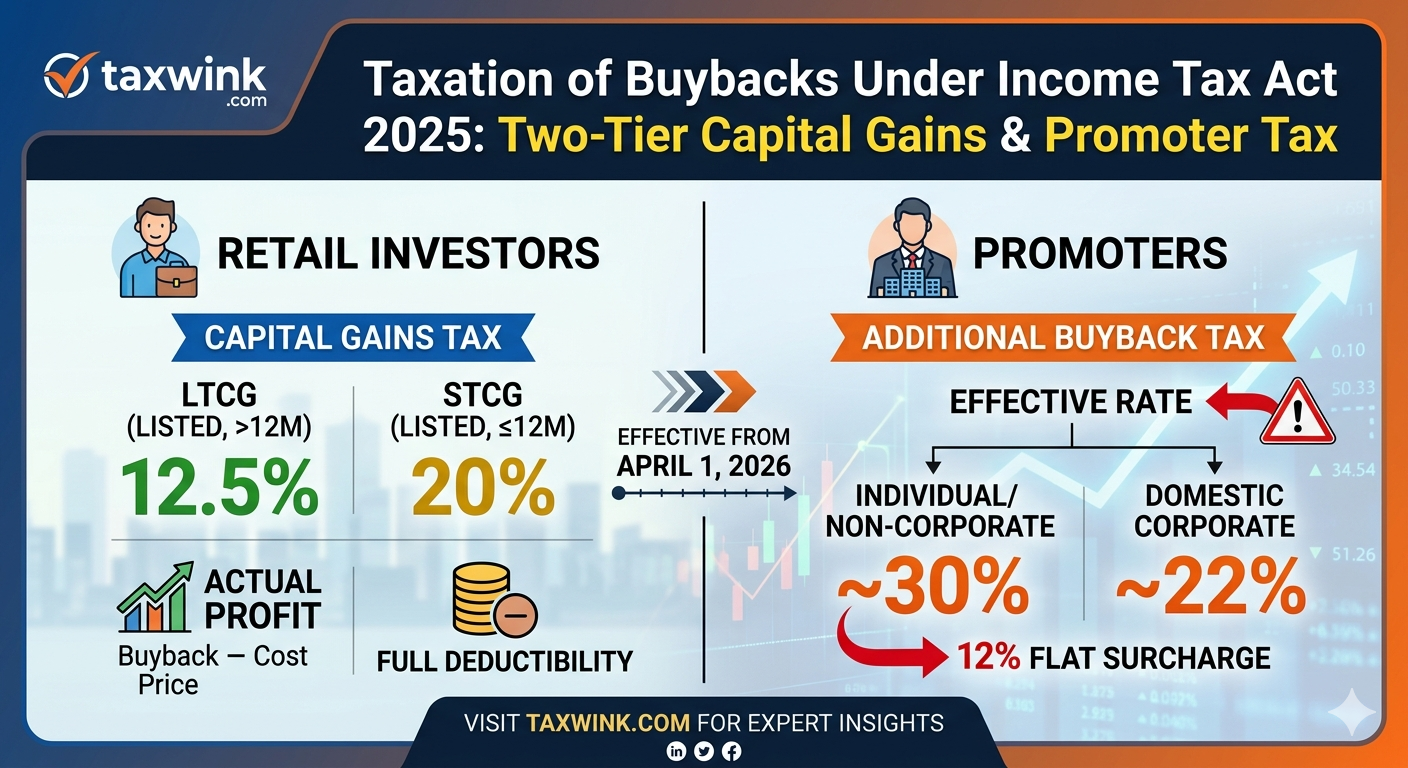

For Ordinary (Non-Promoter) Shareholders

If you are a regular investor — retail, institutional, or otherwise — and you are not a promoter of the company doing the buyback, the rules are now straightforward and equitable:

- Buyback proceeds are taxed as Capital Gains

- Tax is charged only on your actual profit (buyback consideration received minus cost of acquisition)

- The holding period determines whether it is Short-Term Capital Gains (STCG) or Long-Term Capital Gains (LTCG)

- LTCG rate (for listed shares held > 12 months) = 12.5% under Section 196 of the IT Act 2025

- STCG rate (for shares held ≤ 12 months) = 20%

- Normal surcharge provisions apply based on your total income

Illustration: You purchased 500 shares of ABC Ltd at ₹200 each (cost = ₹1,00,000) in April 2023. ABC Ltd announces a buyback in June 2026 at ₹300 per share. You tender all 500 shares and receive ₹1,50,000.

- Capital gain = ₹1,50,000 − ₹1,00,000 = ₹50,000

- Holding period = more than 12 months → Long-Term Capital Gain

- Tax @ 12.5% = ₹6,250

Under the old deemed dividend framework, you would have been taxed on the entire ₹1,50,000 at your slab rate. At 30%, that was ₹45,000. The saving is ₹38,750 on the same transaction. The relief for retail investors is substantial and the correction was long overdue.

For Promoters — The Additional Buyback Tax

While the government has given retail investors significant relief, it was concerned that company founders and promoters — who largely influence the decision to conduct a buyback — could use this route to exit at the concessional 12.5% LTCG rate instead of paying higher taxes on their distributions.

To address this, the Finance Act 2026 has inserted a special additional income tax for promoters under the amended Section 69 of the Income Tax Act 2025.

The effective tax burden on promoters from a buyback, as stated in the Finance Act 2026 Explanatory Memorandum, is:

|

Category of Promoter |

Effective Tax Rate on Buyback Gains |

|

Non-Corporate Promoter (e.g., individual founder) |

~30% |

|

Domestic Corporate Promoter (e.g., parent company) |

~22% |

Additionally, the Finance Bill 2026 as passed by the Lok Sabha specifies a flat 12% surcharge on the additional income tax payable by promoters, irrespective of the total income level. Importantly, this 12% surcharge applies only to the additional income tax component, not to the entire income of the promoter.

Who is a Promoter for this purpose?

- For listed companies: as defined in Regulation 2(k) of the SEBI (Buy-Back of Securities) Regulations, 2018

- For unlisted companies: as defined in Section 2(69) of the Companies Act, 2013, or key directors/controlling shareholders

What This Means for Corporate Strategy

The two-tier system has material implications for how companies think about buybacks:

Companies will now use buybacks for genuine capital management, not promoter exits. With promoters facing an effective tax rate of 30% on buyback gains versus 12.5% on open-market sales, it makes little financial sense for promoters to use buybacks as a personal liquidity mechanism. We should expect buybacks to increasingly be used for their stated purpose: returning genuine surplus cash to the wider shareholder base, reducing equity base, and improving EPS.

Retail investor participation will increase. The simple, equitable capital gains treatment makes buybacks far more attractive for retail shareholders. The "dead loss" problem of Phase 2 — where your cost of acquisition sat as a useless capital loss — is gone. Investors can now model buyback tax liability accurately and make rational participation decisions.

SEBI may reintroduce open market buybacks. SEBI has already released a consultation paper proposing to reintroduce the open market buyback route through stock exchanges. The regulator has explicitly stated that the earlier concern about "tax-induced inequity among public shareholders now stands addressed" under the new framework. This could open a new, more liquid and flexible method of buybacks for companies in addition to the existing tender offer route.

Key Sections at a Glance

|

Provision |

IT Act 2025 Section |

Position |

|

Definition of dividend (buyback removed) |

Section 2(40)(f) — clause omitted |

Buyback no longer = dividend |

|

Capital gains on buyback |

Section 69 (amended) |

Capital gains treatment for all |

|

Additional tax on promoter buyback gains |

Section 69 (new sub-section) |

Additional levy on promoters |

|

LTCG rate on listed shares |

Section 196 |

12.5% |

|

STCG rate on listed shares |

Section 195 |

20% |

|

Surcharge on promoter additional tax |

Finance Act 2026 amendment |

12% flat |

Practical Checklist for Investors and Advisors

Before participating in a buyback or advising a client, verify the following:

- Are you a promoter? If yes, calculate the additional tax liability before tendering shares. The effective rate of 30% may make an open-market sale a better option.

- What is your holding period? Shares held over 12 months from date of allotment/purchase will qualify as long-term, attracting the concessional 12.5% LTCG rate.

- What is your cost of acquisition? Under capital gains treatment, this is now directly deductible from buyback consideration. Ensure you have proper records — purchase contract notes, demat statements, allotment letters.

- DTAA considerations for non-residents: With buyback now treated as capital gains (not dividend), the applicable Article in tax treaties changes. Non-resident shareholders must revisit which DTAA article applies and whether India can tax the gain.

- Loss carry-forward clean-up: If you had recognized a capital loss from a Phase 2 buyback (1 October 2024 – 31 March 2026) under the old deemed dividend regime, consult your CA on whether transitional provisions allow any relief.

Conclusion: A Long-Overdue Correction

The Finance Act 2026 amendment to Section 69 of the Income Tax Act 2025 marks a rational and investor-friendly correction to one of the most criticized provisions of recent years. Taxing shareholders on the entirety of buyback proceeds — instead of just the actual gain — was both economically irrational and deeply inequitable. The government has corrected this.

The two-tier structure — relief for retail investors, stricter levy for promoters — strikes a reasonable balance between investor protection and preventing misuse of the buyback route as a low-tax promoter exit mechanism.

For retail investors, buybacks are now a genuinely tax-efficient exit option compared to open-market sales of large volumes. For promoters, the calculus has changed — and changed significantly.

As SEBI explores reintroducing open market buybacks through stock exchanges, and as companies recalibrate their capital allocation strategies under the new law, the buyback landscape in India is entering a new, more mature phase.

Stay updated. Consult your tax advisor. And when the next buyback announcement hits your inbox, you now know exactly what the tax bill looks like.

This blog is for informational purposes only and does not constitute legal or tax advice. Please consult a qualified Chartered Accountant or tax professional for advice specific to your situation.